6 Debt Relief Options: What Are the Risks to Consider?

When you’re in debt, it can feel as though you are powerless and adrift without choices. Fortunately, you have several avenues of debt relief – but they do all come with consequences. Let’s take a look at what you can do to get out of debt, and the results of those options.

Financial Counselling

As soon as you realize you’re in over your head with debt, you should speak with a financial counsellor. This costs you nothing, and they can help you navigate the difficult path ahead. By comparing the financial outlook of each option as it affects your situation, you’ll be able to make a decision about your financial future – armed with facts and figures and the help of your counsellor.

Consequence:

- This government-sponsored option has the least amount of risks. It’s not a credit provider, but helps you find option through their network of services.

- Long waiting periods to get assistance

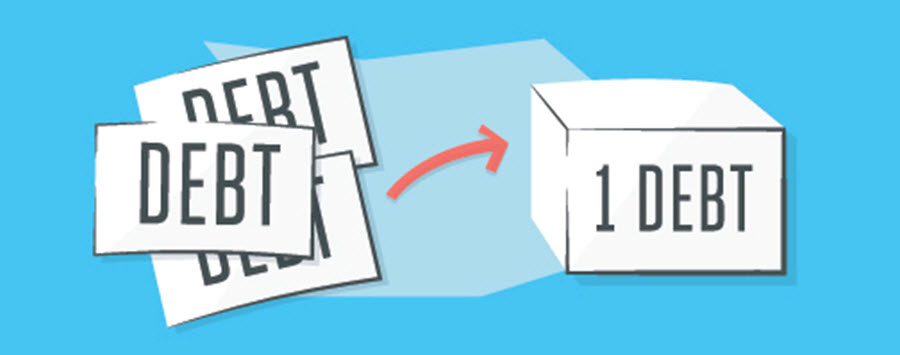

Debt Consolidation

Debt consolidation allows you to exchange multiple debts into one monthly payment. This does eliminate the hassle of having multiple payments over the course of the month.

Consequence:

- Time in debt may be longer

- If accounts aren't closed, there is the temptation to use credit again

- Interest rate may increase over time

Short-term Loans

You can get a regular loan from a bank, if you have good credit or specialist lender is your credit impaired. Use the money to pay off your debt, then pay off your bank loan over time.

Consequences:

- Depending on the loan, it may not be financially beneficial (lower repayment buy pay more in interest).

- Not everyone qualifies

- Terms of loan my be inflexible

Family Loans and Crowdfunding

If your debt problem is short-term or occurs as the result of one particular expense, consider borrowing from a family member or friend or starting a crowdfunding campaign to relieve the debt.

Consequences:

- If you don’t pay your family member or friend back, it could ruin your relationship with them.

- Crowdfunding options like GoFundMe are meant to help, and people do not expect repayment.

- Crowdfunding sites usually take fees from your total.

Bankruptcy

If you’re completely in over your head and have no immediate solution for solvency, bankruptcy is an option. With bankruptcy, you have to work with a trustee who manages your financial decisions and the bankruptcy process for you.

Consequences:

- Bankruptcy affects your employment options.

- Bankruptcy negatively impacts your business (if you own one).

- Your credit is affected by bankruptcy for five years, or two years after your bankruptcy ends (whichever happens later).

What Happens When You Deal With Your Debt?

Once you take action to tackle your debt, you’ll notice some positive consequences as well:

- Reduced amount of phone calls, letters, and other communications from creditors and collectors.

- You’ll likely feel better about having solved the problem.

- Depending on which method you choose to solve the debt issue, you could create an opportunity to improve your credit score – or prevent it from taking a further dive.

Have you dealt with debt in any of these ways? Let us know about your experiences in the comments.