The Art of Debt Stacking

Debt stacking, snowball, upside down pyramid, whatever you want to call it, you can pay off your debt quickly, if you utilize this method correctly. Paying off debt frees up extra money each month that you can use to invest, save for retirement or spend on enjoying life. If you have several debt payments, it can easily feel overwhelming. Learning to debt stack is a great way to make dents in your debt faster and establish some money skills.

How it works:

The idea of debt stacking it to pay off your debts systematically one at a time using money you are already spending on paying off debt. Ideally, you would not have to add any extra money to your debt payments after your initial push.

The first step is to list all of your debts in ascending order by balance. So list your lowest debt (balance) first, then second etc. For example:

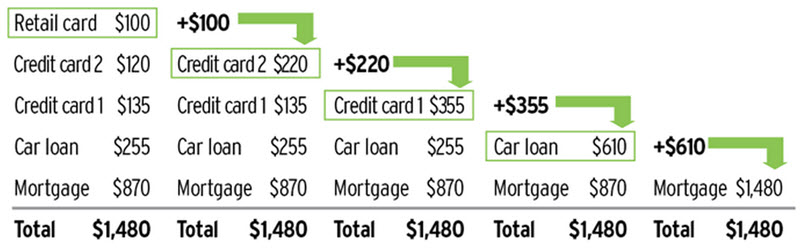

Debt 1: $2500 credit card with a monthly payment of $150 + $100 extra you find in the budget

Debt 2: $5000 credit card with a monthly payment of $300

Debt 3: $15,000 car loan with a monthly payment of $250

Debt 4: $150,000 mortgage with a monthly payment of $950

Total: $1750 per month

Your first line of duty would be to pay off your first credit card. Cut back on other spending and add an extra $100 a month to the first payment (because if you are only paying the minimum balance it will take forever to pay off). So, your first debt would now be $250 per month. Every other debt payment stays the same.

Once you pay off the first debt you take the $250 (the original $150 plus, the extra $100 you found in your budget), you paid on your first debt and add it to your second debt. You are now paying $550 per month towards your second debt and your monthly debt payments stay at $1750 per month.

Once you have paid off your second debt, you have your car payment and your mortgage left. Take the money you were already paying towards your second debt and add it to your third debt. So $550 to the $250 car payment= $800. Keep doing this until all of the money you were paying on debt is going into your mortgage. Instead of paying $950 per month, you will pay $1750, which will allow you to pay of the rest of your mortgage in half the time.

Why it works:

Once most people pay off a debt, they just start spending that extra money on nonessentials. When you use money, you are already spending on debt, to add to other debt payments it compounds quickly and sucks away at balances fast. You are already spending the money, so you won’t even miss it from your budget.

You can still use this system even if you cannot afford an extra $100 to add to your first debt. Any extra you can add will help you pay it off faster, but you can still do it by sticking with your original payments. Just remember to take that payment and add it to another debt as you finish paying the bill.

Some financial experts suggest paying off the highest interest rates first. However, you may find it more motivating to tackle smaller balances because you will see results faster.

For other debt, elimination strategies visit our debt relief page and see what tactic might work for you. Find multiple options, which include free and low cost professional services.