The Cost of a Low Income Loan

When times get tough, you might need a loan. If you have a low income, you’ve probably investigated multiple low income loan options. When it comes down to doing the loan, it’s important to examine the true cost of it. That involves looking at several qualification and repayment factors.

Investment of Time (the price of your time and effort)

Each lender will have its own approval and qualification process, with some being easier than others. Online lenders are typically quicker than in person. Borrowing from your bank can also be a quick process. See a list of low income loans which are generally a quick process.

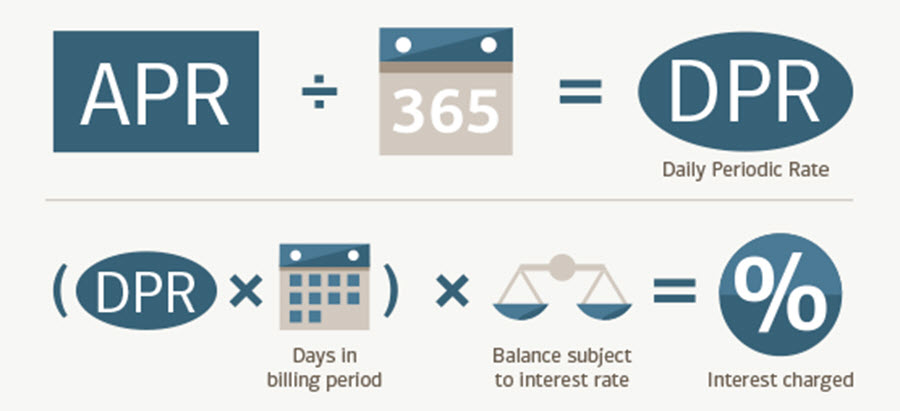

Interest Rate (Review calculators to understand costs)

It’s vital to consider the interest rate on the loan. Many smaller short-term loans have high interest rates. Often pitching what the repayment may be versus the costs of the finance. However, do to all the publicity around expensive small loans, many lenders are now providing full transparency in regards to all costs associated with finance.

Payday loans are the least advisable choice, assuming you have alternatives. Their interest rates are extremely high and repayment terms are steep – they’re literally banking on your next paycheck and are generally considered to be predatory. These loans come at a cost, with interest rates beyond that of even credit cards.

Certain states have outlawed them all together and others have set caps on the amount of interest they can charge – learn more.

Borrowing from a friend or family member might come with strings, but it’s usually a lower cost option with more forgiving repayment terms.

Bank loans vary greatly – especially when you’re looking at personal loans. They tend to be more reasonable than a payday loan, but the application and disbursement takes some time to go through. If your need is dire, you might not have the luxury of that time.

Penalties (Read the fine print)

It’s also important to consider the penalties if you fail to repay your loan. Many lenders demand high penalties for being late on your loan repayment – even once. Those fees can add up and you may end up in a landslide of debt.

Additionally, did you know that some lenders will punish you by paying your loan back early? It’s true! Read the fine print.

Loan Application Fees (Read the fine print and potentially negotiate)

Especially with private lenders, expect an application fee. This covers the work the bank has to do to process your application.

Make the Worksheet

When considering your different loan options, make a worksheet. Make sure to include the different costs:

- Time

- Interest

- Application Fees

- Penalties

- Other expenses, such as transportation costs to and from the bank, especially if you need to take public transit

When you’re in need, it’s difficult to think clearly sometimes. That’s why having it all tallied up on a spreadsheet can help. Plus, you can bring this sheet in to your financial counsellor if you need help evaluating the options.

Whatever decision you make, ensure it’s a well-researched one.