Understanding Overdraft Accounts – Are They Worth It?

Don’t let an overdraft take you overboard

When you need a little extra cash, it’s tempting to just overdraft on your bank account to complete the purchase you intend to make. Take caution- overdraft is essentially another type of credit, attracting fees and charges.

- How do overdrafts work?

- What to look out for

- How to manage your overdraft

- Read your contract

How do overdrafts work?

An overdraft is a credit for your bank account that takes care of your short-term needs, and you can apply for one or set it up as part of your account.

Unarranged overdrafts

When you accidentally overdraft, it means you’ve taken more money out of your account than was there, landing you with a negative balance in your bank account.

There’s a solid chance your banking institution will give you the money, creating a debt. It may charge a standard overdraft fee of about $36 for each transaction that posts while your account remains with a negative balance. Your bank will expect a payment to cover the overdrawn funds immediately. You can always check the paperwork you’ve received when you established your bank account to understand your bank’s overdraft process.

If you have had a long-standing account with your banking institution, or have established yourself as a valued customer, you may find that the bank doesn’t charge you an overdraft fee. Or if you are, you’re likely able to make a call to them and negotiate that this fee be waived if it’s a one-time offense.

Arranged overdrafts

You can arrange an overdraft on your personal account by linking it to another checking account or a credit card. That way, if you were to spend more than you have, the insufficient funds would be paid through a separate account or your credit card, and you’ll avoid the overdraft fees.

Keep in mind, whatever balance is transferred to your credit card will accrue interest in the same way as other purchases on the card. If you utilize this overdraft function too often, you may find yourself increasing your debt to a point where your credit score is affected. The good new is, it won’t reflect as an issue with your bank account.

Things to look out for

Overdraft protection is great for paying bills in full, and not having any returned check fees. However, this form of protection can often seem encouraging to spending money you don’t have. Here are some things to watch for.

Fees

Fees can get out of hand quickly, sending your account into much worse condition than when you first reached a negative balance.

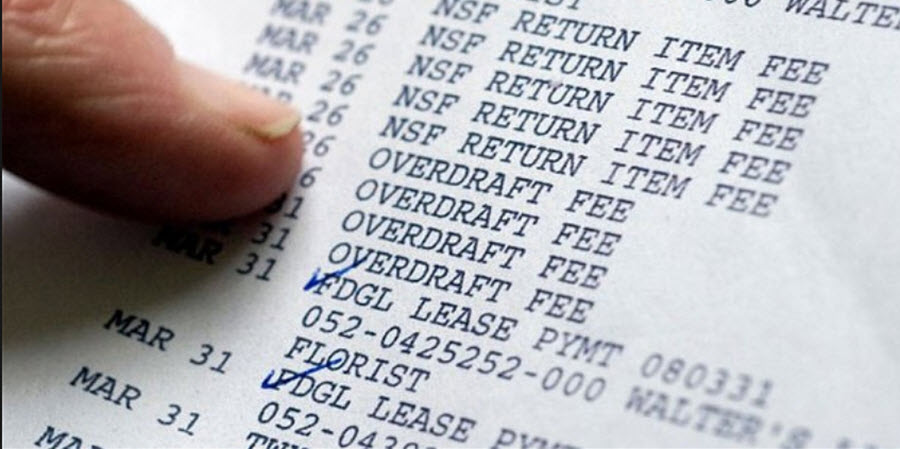

- Insufficient funds fees (NSF) – If you get a negative balance, and fail to recognize other auto pay drafts that may be scheduled soon after, you can have a $36 fee for every single transaction that posts after your account becomes overdrawn.

- Interest from overdraft protection on your credit card- if you rely on your credit card for overdraft protection, you agree to pay the interest rate set by the credit card on your goods, services, or bills. Depending on the interest rate and amount that transferred to your card, you may pay more on the balance than the standard overdraft fee from your banking institution.

“Inaccurate” ATM balances

Even if you don’t know what your standard overdraft protection is, some ATMs allow you to withdraw more money than you have in your account. If you’re withdrawing money without checking your account balance, you could unintentionally overdraft.

ATMs often show your available balance, but it might not be accurate. The pending transactions on your account may not be reflected in that balance.

How to manage your overdraft

Find out ways to avoid fees and use your overdraft responsibly. Below are numerous examples of how to control costs and not fall into serious debt or get slugged with high fees.

Don’t bite off more than you can chew

If given the option, choose the lowest overdraft limit possible and avoid overspending.

Find out what you will owe

Get a complete list of the fees you’ll incur if you overdraft.

Repay your debts quickly

Sort out the timeline of your overdraft. Banking institutions often have a limit for how long an account can remain with a negative balance before it’s turned over to a collection agency.

Avoid lending to others if possible

If helping another person financially means you may overdraft, think twice. You risk owing more money than you have. See our article on loans involving family and friends.

Look for patterns in your spending

If you constantly overdraft, pause and evaluate how you spend your money. See our budgeting tips for how to make better use of your funds.

With smaller purchases, you might discover a credit card is easier to manage and will end up having fewer total fees and interest, compared with your overdraft fees. With larger purchases, consider applying for a personal loan.

Read your contract

Always check your terms and conditions before signing up for an account.

Check your credit providers’ and banking institutions’ practices for account fees, interest, overdraft protection, waivers, and more.

An overdraft may appear convenient, but the resulting fees can really put a dent in your wallet. Explore other credit options before entertaining an overdraft. There may be other options that are much cheaper and better suited to your situation.